Do not assume your existing FEHB plan will stay the same in 2025. tommy/Getty Images

Last-minute advice for the 2025 open season

Things you need to consider before the annual window when federal employees can enroll in or make changes to their health benefits closes on Dec. 9.

FEHB Open Season ends on Mon., Dec. 9. Here’s what you need to consider before then:

Your Current Plan

Don’t assume your existing FEHB plan will stay the same in 2025. Here’s how it could’ve changed:

- Premium – The average enrollee share of premium is increasing 13.5%, which means most plans will cost more. Of the 144 plans available in 2024 and again in 2025, premiums will decrease in 28 plans, stay the same in 5 plans, increase below the average in 69 plans, and above the average in 42 plans. How is your premium changing? This is a for-sure expense, so take time to understand how it compares to other plans and determine if yours is still the right fit.

- Benefits – Many plans have benefit changes in 2025, and they could impact your decision to remain enrolled in your current plan. These include pre-authorization requirements, new benefits that have never been available before, or modifications to existing ones. To review these updates, refer to section 2 of the official FEHB plan brochure. Here are a couple of examples of changes for 2025:

- All GEHA plans have added doula coverage

- BCBS Basic is increasing the catastrophic limit, and increasing the member cost share for specialist visits, inpatient and outpatient hospital, brand name drugs, and more.

- Doctors & Prescription Drugs – The status of providers and prescription drug coverage can change each year. Be sure to visit your plan’s website to confirm that your current doctors will remain in-network and that your prescription drugs will continue to be covered. Also, check the out-of-pocket costs for your medications to ensure there are no major price increases.

For example, there is a formulary change with BCBS Basic that will significantly increase the out-of-pocket cost next year for Wegovy, a GLP-1 weight loss medication. Due to a tier change, a 28-day supply of the .25mg injectable at a CVS in the Washington, D.C., area will rise from $60 this year to $767.38 next year.

Plan Availability

There are a few FEHB plans that won’t be available next year: CDPHP and HIP in New York; Dean Health in Wisconsin; and Blue Shield of California Access+ HMO and Healthnet of CA Basic in Northern California.

Additionally, there could be service area changes that could alter the availability of some plans. UnitedHealthcare Choice Open Access, Healthnet of California in Southern California, Health Alliance Plan in Michigan, and Geisinger Health Plan, Standard and Basic, have all reduced their service areas. If you’re impacted by these plans leaving, you’ll need to choose a new FEHB plan this Open Season. If you don’t, OPM will auto-enroll you in the least costly national PPO plan, GEHA Elevate.

Two new FEHB plans will be available in 2025: Sharp Health Plan in the San Diego, CA area, and Western Health Advantage in areas outside of San Francisco, CA. Additionally, Compass Rose has lifted its enrollment restrictions, making its High and Standard plan accessible to all FEHB enrollees.

Consider Switching Plans

Less than 5% of federal employees or retirees switch plans during any year, and many have kept the same one for years. If you’re that someone, and you haven’t looked at your options in a while, now is a good time to see if a new plan could offer you savings.

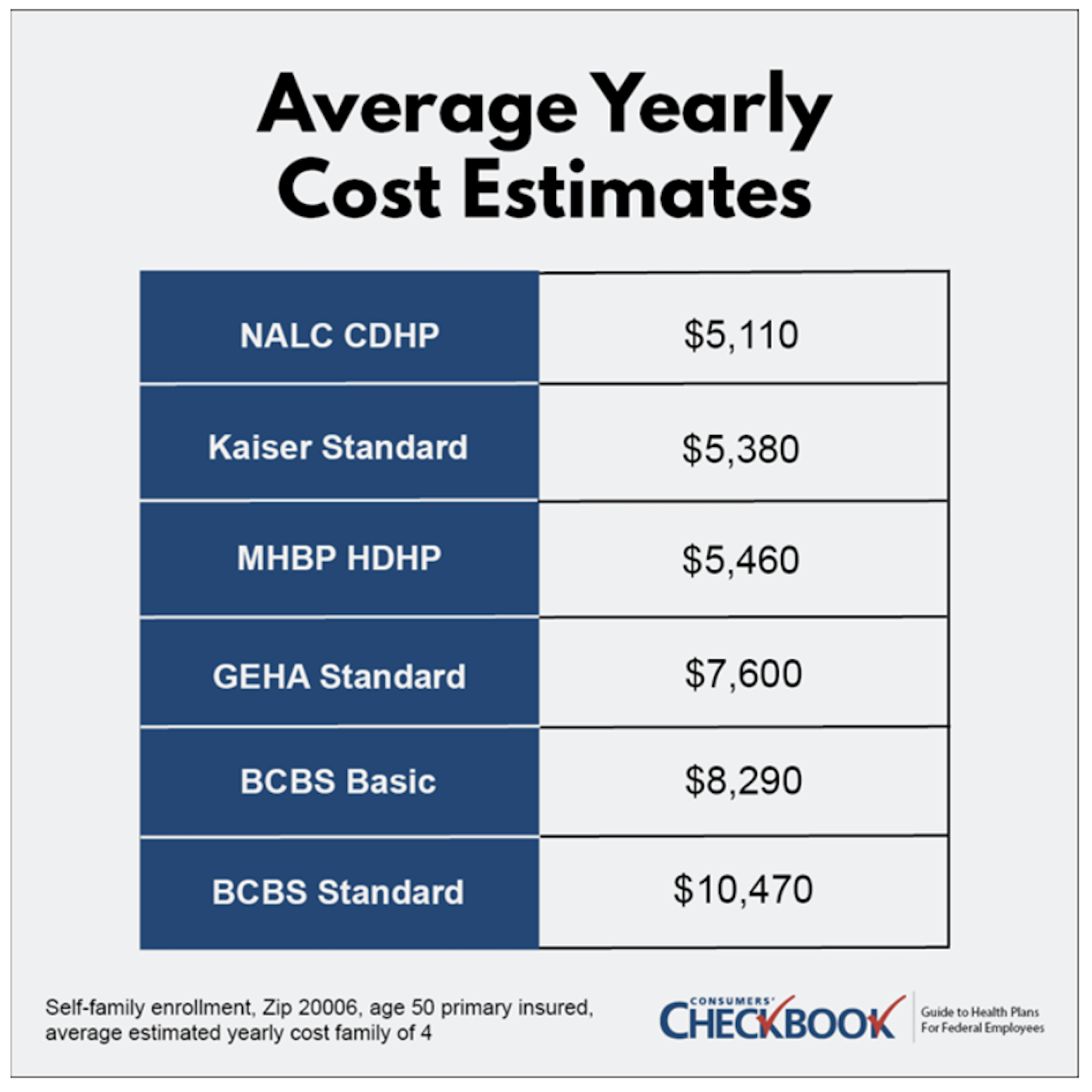

For 46 years, Checkbook’s Guide to Health Plans for Federal Employees has ranked plans on estimated total cost based on user information—age, family size, and expected healthcare usage. The benchmark ranking shows big price differences among plans for plan year 2025.

For example, a family of four in the Washington, D.C., area with age 50 primary insured and average healthcare expenses could save $5,360 in estimated costs switching from BCBS Standard to NALC CDHP.

How to Save Money on Healthcare Expenses

With a 13.5% increase in the average enrollee share of FEHB premiums for 2025, federal employees should be looking for ways to save money on healthcare expenses. But only 20% of federal employees use a flexible spending account.

All federal employees will have some predictable healthcare expenses next year—dental care, vision care, planned medical visits, prescription drug refills, or over-the-counter pharmacy items. Through funding from payroll contributions before taxes, paying for approved healthcare expenses with the FSA will save you about 30%.

Employees can contribute up to $3,300 in 2025, but you must be somewhat careful in budgeting as only $660 of unused funds can be rolled over into a new plan year. Employees with an HSA aren’t allowed to have a healthcare FSA, but they can still set up a limited expense FSA for dental and vision expenses, which is a good idea to help keep HSA funds invested. You must renew your enrollment every Open Season to keep your FSA. You can enroll and learn more at FSAFEDS. FSA Open Season also ends December 9th.

The Final Word

Even if you want to keep your existing FEHB plan, you need to confirm that there are no major changes that might alter your enrollment decision. Go to section 2 of the plan brochure to learn about benefit changes, understand how the premium has changed, and confirm that your doctors will still be in-network and your prescription drugs will be covered.

Make sure to consider other plans. You could save thousands of dollars next year switching to a cheaper plan that has similar coverage.

Take advantage of the FSA. With higher premiums, this is an easy way to save on your healthcare costs.

Open Season ends on Dec. 9.

Kevin Moss is a senior editor with Consumers’ Checkbook. Watch more of his free advice and check here to see if your agency provides free access. The Guide is also available for purchase and Government Executive readers can save 20% by entering promo code GOVEXEC at checkout.